Many developing countries are struggling to recover from the pandemic despite a record-high level of official development assistance (ODA) and a strong rebound in global foreign direct investment (FDI) and remittance flows. Among other challenges, developing countries are battling record inflation, rising interest rates and looming debt burdens. With competing priorities and limited fiscal space, many are finding it harder than ever to recover economically. With the pandemic far from over and stark disparities in vaccine distribution among countries, there is also the threat of a “two-tiered” COVID-19 recovery. To build back better from the pandemic and rescue the Sustainable Development Goals, a full-scale transformation of the international financial and debt architecture will be required. The world is facing a multitude of crises across the social, health, environmental, and peace and security spectrums. To find lasting solutions, international cooperation must be scaled up – urgently. To stay ahead of crises, significantly more investment in data and statistics will be necessary.

Official development assistance has reached a new high, largely due to COVID-related aid, but still falls short of the target

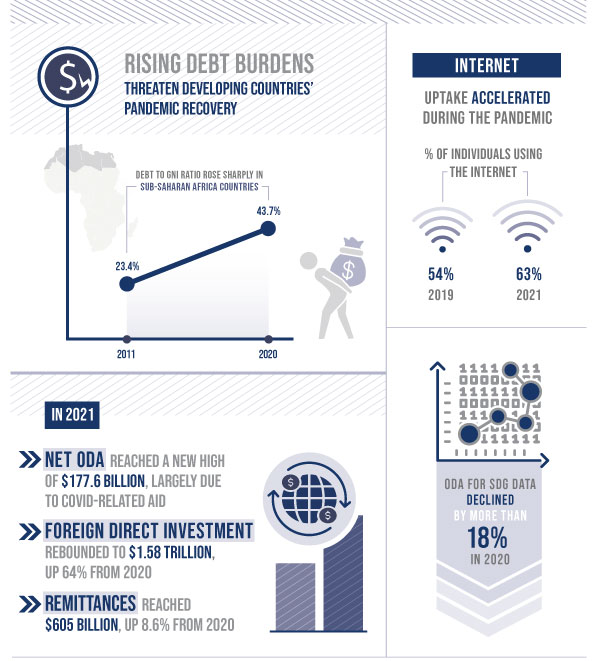

In 2021, net ODA flows by member countries of the Organisation for Economic Co-operation and Development’s (OECD) Development Assistance Committee (DAC) amounted to $177.6 billion, an increase of 3.3 per cent in real terms from 2020. This level of ODA represented 0.33 per cent of donors’ combined gross national income (GNI), reaching a new peak. Yet it still fell short of the 0.7 per cent target, and is not enough to enable developing countries to get back on track in meeting the Sustainable Development Goals targets. The increase is mostly due to DAC members’ support for COVID-19-related activities (including prevention, treatment and care), with an initial estimate of $18.7 billion. Within this total, ODA for COVID-19 vaccine donations was $6.3 billion (or 3.5 per cent of total net ODA), amounting to nearly 857 million doses for developing countries.

Since 2015, net ODA has increased by 20 per cent. Despite fiscal pressures in all countries, ODA peaked in 2020 and again in 2021. The ongoing war in Ukraine is having a direct impact on ODA in 2022, due to increased spending on refugees. Military assistance to Ukraine and rising military spending by European nations is not considered ODA.

However, it could lead to a sudden reshuffling of budgets and threaten development aid to the world’s poorer countries at a time when it is urgently needed.

Components of net official development assistance flows, 2015-2021 (billions of constant 2020 dollars)

The importance of data and statistics for sound decision-making has never been clearer, but funding for this sector has stagnated

Timely and high-quality data have proven to be critical in guiding decision-making for development, particularly during the pandemic. In 2021, 150 countries and territories reported implementing a national statistical plan, up from 132 in 2020, with 84 of those fully funded. The pandemic has delayed the development of new plans worldwide, meaning that many national statistics offices are implementing expired plans that may not fully cover their evolving development objectives.

A recent survey found that the majority of national statistics offices in low-income countries experienced either moderate or severe delays in budget disbursement in 2021. Many of them relied on development aid from external sources, which has decreased during the pandemic, to implement their work programme. Over the next three years, they expect to face the most significant funding shortages in business and agricultural censuses, as well as population and housing censuses.

Early analysis indicates that ODA for data and statistics amounted to $650 million in 2020, a slight decline from $662 million in 2019. The overall trend in funding for this sector has remained stagnant at 0.3 per cent of total ODA. Moreover, excluding a significant rise in funding for health data, funding received for other statistical activities that are considered fundamental declined by 18 per cent. Funding for data specific to the Sustainable Development Goals, such as gender data and climate data, declined even more than that in 2020. This indicates that even the most basic data activities were quickly deprioritized at the beginning of the pandemic, leading to serious data gaps and backlogs in countries most in need.

The pandemic has added extra weight to the debt burdens of low- and middle-income countries

Total external debt stocks of low- and middle-income countries rose by 5.3 per cent in 2020 to $8.7 trillion. This was driven by an increase in long-term debt, which rose by 6 per cent to $6.3 trillion. As a result of the global pandemic, external debt ratios further deteriorated as the pace of external debt accumulation outstripped growth of export earnings in most low- and middle-income countries. In low-income countries, the total public and publicly guaranteed debt service to export ratio rose from an average of 3.1 per cent in 2011 to 8.8 per cent in 2020. The worsening of debt indicators was widespread and affected countries in all geographic regions. Countries in sub-Saharan Africa have seen the most pronounced deterioration in debt indicators: the ratio of debt to GNI rose from an average of 23.4 per cent in 2011 to 43.7 per cent in 2020, and the average debt-to-export ratio tripled over the same period.

Debt service to export ratio by income group, 2011–2020 (percentage)

Internet use has surged, prompted by the pandemic, although poorer regions still lag behind

Since the emergence of COVID-19, the Internet has become vital for working, learning, accessing basic services and keeping in touch. The latest data show that uptake of the Internet has accelerated during the pandemic. In 2019, 4.1 billion people (or 54 per cent of the world’s population) were using the Internet. The number of users surged by 782 million to reach 4.9 billion people in 2021, or 63 per cent of the global population. In 2020, the first year of the pandemic, the number of Internet users grew by 10.2 per cent. This was the largest increase in a decade, driven by developing countries, where Internet use went up by 13.3 per cent. In 2021, growth returned to a more modest 5.8 per cent, in line with pre-crisis rates. The number of Internet users in LDCs increased by 20 per cent and accounted for 27 per cent of the user population between 2019 and 2021.

Fixed broadband subscriptions continue to grow steadily, reaching a global average of 17 subscriptions per 100 inhabitants in 2021. In LDCs, despite double-digit growth, fixed broadband remains a privilege of the few, with only 1.4 subscriptions per 100 inhabitants.

Proportion of individuals using the Internet, 2021 (percentage)

*Excluding Australia and New Zealand.

Global foreign direct investment rebounded strongly in 2021, but flows to the poorest countries showed only modest growth

Global foreign direct investment flows rebounded strongly in 2021, reaching $1.58 trillion, an increase of 64 per cent compared to 2020. Recovery was highly uneven across regions, however. Developed economies saw the biggest rise, with FDI reaching an estimated $746 billion in 2021 – more than double the 2020 level. FDI flows in developing economies increased by 30 per cent, to nearly $837 billion. Flows in LDCs saw a more modest growth of 13 per cent. Inflows to LDCs, landlocked developing countries and small island developing States combined accounted for only 2.5 per cent of the world total in 2021, down from 3.5 per cent in 2020.

International investment in SDG-related sectors in developing countries increased by 70 per cent in 2021. Most of the growth came from renewable-energy and energy-efficiency projects. However, the share of total SDG investment in developing countries that went to LDCs decreased from 19 per cent in 2020 to 15 per cent in 2021.

Remittance flows to poorer countries remain robust, buttressed by strong economic activity and employment levels in many host countries

In 2021, remittance flows to low- and middle-income countries reached $605 billion, a robust growth of 8.6 per cent from 2020. For a second consecutive year, remittance flows to these countries (excluding China) surpassed the sum of FDI and ODA. This significant rise was fuelled primarily by migrants sending money home to families facing economic hardships during the pandemic. Strong economic activity and employment levels in many large host countries that implemented fiscal stimulus programmes aided this growth. The cost of sending money across international borders continued to remain high, at 6.0 per cent on average, double the 3 per cent target.

It is projected that remittance flows will increase by 4.2 per cent to reach $630 billion in 2022, less than half the growth seen in 2021. This decline is a direct impact of the crisis in Ukraine. Remittances to that country are expected to rise by over 20 per cent in 2022. However, many Central Asian countries dependent on the Russian Federation will likely see a decline in remittance flows.